The U.S. dental bone grafting industry is forecast to increase in size owing to factors such as the increasing number of dental implant procedures being performed. (Image: 2j architecture/Shutterstock)

NEW YORK, U.S.: Dental bone grafting has become an important and common step in the dental implant procedure. Advancements in allograft, xenograft and synthetic bone graft materials have positioned them as suitable alternatives to traditional autologous bone grafts, and this has created a thriving market for dental biomaterials. Although demand declined significantly in 2020 owing to the rippling economic effects of the COVID-19 pandemic, it is expected to recover quickly alongside the overall demand for dental implants.

Notable trends accelerating growth in this market include the increasing number of dental implant procedures performed. There is also a growing body of evidence suggesting that most (if not all) dental implant procedures could benefit from a bone graft.1 Although the dental bone graft substitute (DBGS) market faces some minor headwinds in commoditization effects and short-term pandemic-related constraints, the long-term outlook and secular growth trends remain positive.

Trend 1: Growth in implant market; stronger scientific support

The number of implants being placed with bone graft substitutes is increasing, and a growing body of evidence suggests that most dental implant procedures could benefit from a bone graft. (Image: iData Research)

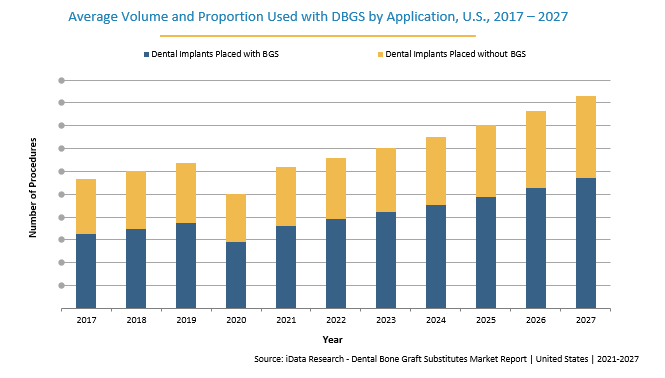

The percentage of dental implants placed with DBGS in the U.S. is forecast to grow from 58% in 2020 to over 60% in 2027, according to iData Research’s new report on the U.S. DBGS market. Because the two markets are closely related, the same growth trends that drive the demand for dental implants will also contribute to growth in sales of dental biomaterials. These trends include an aging population that is more prone to ailments like edentulism, a growing number of dentists trained in implant dentistry, improved consumer accessibility owing to industry consolidation, and stronger value propositions offered by shrewd pricing strategies.

In addition, there is growing clinical research suggesting that bone graft substitutes perform as well as autologous grafts with regard to bone formation, eliminating the need for costly and uncomfortable secondary grafting procedures.2 This level of rigorous scientific documentation lends credence to manufacturers’ own clinical trials and reinforces the value proposition of DBGS materials in implant dentistry.

Trend 2: Slowing innovation and bundling of DBGS

Innovations in bone grafting products are most often driven by advancements in the much larger orthopedic market, before trickling down into dental applications. In recent years, innovation has slowed in both the orthopedic and dental biomaterial markets, particularly with regard to bone graft substitutes, leaving little room for price growth and product differentiation. Furthermore, parts of the market are heavily fractured owing to hundreds of competitors offering similar products, which exerts downward pressure on prices and market value.

Put together, the two effects of commoditization

and bundling present a moderately bullish case for the DBGS market

Leading manufacturers have instead turned to leveraging their strong positions in the marketplace by employing bundling strategies to mutually reinforce demand for both dental implants and biomaterials. Because demand for dental biomaterials is largely driven by specialists, who typically order large volumes of dental implants in bulk, companies with strong brand recognition across the dental supply industry, like the Straumann Group, Zimmer Biomet and BioHorizons, have capitalized on this imbalance by bundling DBGS and implant products.

Put together, the two effects of commoditization and bundling present a moderately bullish case for the DBGS market. Although competition and commoditization can threaten stalled growth, strong players in the DBGS and adjacent markets will be rewarded if they are able to continue providing value to end users by offering attractive pricing strategies. The DBGS overall sales value is expected to have shrunk by nearly 21% in 2020 owing to the pandemic-induced economic downturn, followed by a sharp rebound of around 22% in 2021.

Dr Kamran Zamanian is CEO and founding partner of iData Research. He has spent over 20 years working in the market research industry with a dedication to the study of dental implants, dental bone grafting substitutes, prosthetics, as well as other dental devices used in the health of patients all over the globe. (Image: iData)

Trend 3: Innovation opportunities in barrier membranes and regenerative materials

While innovation in DBGS has slowed, there is no evidence of this for dental barrier membranes and dental growth factors. Over the next six years, both markets are projected to grow at an annualized rate of over 6%, following a sharp decline in 2020 and a complete recovery in 2021.

In the barrier membrane supply chain, market leader Osteogenics Biomedical has been consistently releasing new products with promising novel features. In 2019, the company released the RPM reinforced PTFE mesh, which was designed to work like a traditional titanium mesh but with a porous design that provides the added benefits of easier trimming and adaptation. In 2020, Osteogenics announced a distribution partnership with DBGS giant Geistlich Pharma, adding the mesh to Geistlich’s expansive biomaterial portfolio. This move combines the brand recognition of two strong players in their respective markets to reinforce demand.

Currently, manufacturing of dental growth factors is led by four major players: Medtronic, Lynch Biologics, the Straumann Group and ACE Surgical. Each of these companies’ regenerative products is indicated for a slightly different use, though they all generally originated as innovative products for orthopedic applications. Dental growth factor production is still in its early stages of the industry life cycle, and the entire market stands to benefit from new product developments in the orthopedic market. Furthermore, blood derivative growth factors such as platelet-rich fibrin (PRF) are seeing a rise in popularity. Notably, BioHorizons acquired Intra-Lock in 2018, stating in a press release that it was “excited to add the IntraSpin system to [its] portfolio since [PRF] is increasingly used in grafting procedures.”3 Although it is not yet clear that blood derivative growth factors are ready for prime time, an endorsement of PRF products by a major player is a good indication of the market trend.

The impact of COVID-19 on dental bone graft substitutes

William Guo is a research analyst at iData Research. He has been involved in the global research of dental implant and bone graft substitute markets, publishing the reports on the U.S. market. (Image: iData)

The COVID-19 pandemic and subsequent forced business closures ground all dental implant procedures to a halt in early 2020. As dental clinics across the U.S. began to reopen in the latter half of 2020, dentists reported a large volume of pent-up demand for implant (and therefore bone grafting) procedures, which is a promising indicator for a strong recovery.4 Industry leaders remain confident in their respective companies’ fundamentals and expect to recover pre-pandemic sales by the end of 2021 or early in 2022 before resuming previous growth targets.

Demand is forecast to grow

Demand for dental biomaterials will continue to grow alongside the dental implant market for the foreseeable future in the U.S. as well as in 21 other countries, as analyzed by iData Research. Although some segments may be negatively impacted by slowed innovations and increased competitive pressures, the medium- and long-term growth trends remain positive. Major drivers of sales include growth in the related dental implant market, increases in supporting scientific literature, and innovations in dental regenerative products. Like the dental implant market, the DBGS and related biomaterial markets will make a strong recovery from the pandemic-induced market shock and continue a modest growth trend over the forecast period.

Editorial note: A list of references can be obtained from the publisher.

BOSTON, US: In the US, dental care remains largely excluded from medical insurance and separated from public health initiatives that promote prevention. A ...

SILVER SPRING, Md., US: The US Food and Drug Administration (FDA) has finalised guidance on animal studies for dental bone grafting material devices, aiming...

SYDNEY, Australia: This year’s FDI World Dental Congress is going to be one of the premier global dental events of the year, not only bringing the dental ...

The digital dentistry market in Asia Pacific has started to gain traction because of technological advances and the demand for improved precision, although ...

KOBLACH, Austria: Digitisation in the dental industry is unstoppable, heralding change and offering enormous potential. Many dental technicians and dentists...

ATLANTA, U.S.: Vyne Dental, a recognized market leader in health care information exchange and electronic communication management, has announced the ...

TAIPEI, Taiwan: Dental anxiety research has surged over the past three decades, reflecting growing recognition of its impact on oral health and patient ...

COLOGNE, Germany: The International Dental Show (IDS) is already seeing strong demand for its 2027 edition. Shortly after exhibitor registration opened, ...

The use of 3D imaging has become the standard of care for diagnosis and treatment planning for many medical and dental procedures. Such imaging was first ...

Education

Live webinar Mon. 27 July 2026 4:00 am EST (New York)

Brazil / Brasil

Brazil / Brasil

Canada / Canada

Canada / Canada

Latin America / Latinoamérica

Latin America / Latinoamérica

USA / USA

USA / USA

Austria / Österreich

Austria / Österreich

Bosnia and Herzegovina / Босна и Херцеговина

Bosnia and Herzegovina / Босна и Херцеговина

Bulgaria / България

Bulgaria / България

Croatia / Hrvatska

Croatia / Hrvatska

Czech Republic & Slovakia / Česká republika & Slovensko

Czech Republic & Slovakia / Česká republika & Slovensko

France / France

France / France

Germany / Deutschland

Germany / Deutschland

Greece / ΕΛΛΑΔΑ

Greece / ΕΛΛΑΔΑ

Hungary / Hungary

Hungary / Hungary

Italy / Italia

Italy / Italia

Netherlands / Nederland

Netherlands / Nederland

Nordic / Nordic

Nordic / Nordic

Poland / Polska

Poland / Polska

Portugal / Portugal

Portugal / Portugal

Romania & Moldova / România & Moldova

Romania & Moldova / România & Moldova

Slovenia / Slovenija

Slovenia / Slovenija

Serbia & Montenegro / Србија и Црна Гора

Serbia & Montenegro / Србија и Црна Гора

Spain / España

Spain / España

Switzerland / Schweiz

Switzerland / Schweiz

Turkey / Türkiye

Turkey / Türkiye

UK & Ireland / UK & Ireland

UK & Ireland / UK & Ireland

China / 中国

China / 中国

India / भारत गणराज्य

India / भारत गणराज्य

Pakistan / Pākistān

Pakistan / Pākistān

Vietnam / Việt Nam

Vietnam / Việt Nam

ASEAN / ASEAN

ASEAN / ASEAN

Israel / מְדִינַת יִשְׂרָאֵל

Israel / מְדִינַת יִשְׂרָאֵל

Algeria, Morocco & Tunisia / الجزائر والمغرب وتونس

Algeria, Morocco & Tunisia / الجزائر والمغرب وتونس

Middle East / Middle East

Middle East / Middle East

Federico ZunicaRegister now1CELive webinar

Federico ZunicaRegister now1CELive webinar

Dr. Sergio FlorencioLive webinar

Dr. Sergio FlorencioLive webinar

Dr. Cameron Shahbazian DMD MBARegister now1CELive webinar

Dr. Cameron Shahbazian DMD MBARegister now1CELive webinar

Dr. Francesco GrandeRegister now1CE

Dr. Francesco GrandeRegister now1CE

To post a reply please login or register